Aside from a local level or trend variance, the time series of nonstationary processes behave similarly across all sections of the time series, even if they do not vary around a static mean. Because of this, it's possible to model these nonstationary processes as stationary by specifying an appropriate difference (such as the level or slope).

The following results emphasize that models are considered stationary concerning the dth difference in time of the time series. The GWVS and GES may be considered as "time-varying spectra" that expand the PSD of the segment includes and the mean instantaneous intensity of white operations when applied to the under nonstationary phenomenon. A modest weighted GEAF integral ensures that the following approximations (or moments, or a small TF connection spread x) are valid.

Data from a Non-Static Time Series

Data points' means, variance, and covariances are frequently nonstationary or fluctuate over time. Trends, cycles, randomized walks, or a combination of the three can be nonstationary behaviors.

As a rule, it is impossible to model or predict nonstationary data. Nonstationary time series analysis might produce erroneous results by suggesting a connection between two variables that do not exist. The nonstationary data must be turned into stationary data to get trustworthy results.

Nonstationary Processes: Types and Applications

Before we can begin the transformation process, we must first categorize financial time-series data into distinct types of nonstationary operations. We can apply that correct transformation because of this improved knowledge of the processes.

A non-stationary process is exemplified by a random walk, which can have or not have a drift (trends that are constant, positive, or negative, independent of time for the whole life of the series).

Processes that aren't stationary

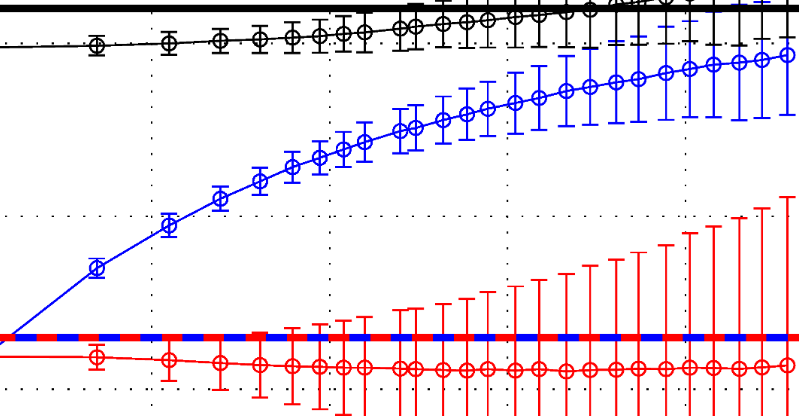

- Nonsensical Paths (Yt = Yt-1 - t) Yt An identically distributed and independent "white noise" component, known as a stochastic component, is added to the last period's value to anticipate the value. At the time, "t." Other names for a random walk include the integration of some order, the stochastic trend of some order, and the stochastic trend of some order. Negative or positive deviations from the mean are possible in this non-mean-reverting process. As time goes on, the variance of a random walk increases and eventually reaches infinity; thus, a random walk cannot be predicted.

- With Drift, Take a Random Walk At this point, we know that each of these values is equal to one plus one plus one plus one. That which is predicted at time "t" will be based on a random walk model, which includes an additional term for white noise (t), and a constant known as the "drift," is known as a random run with a drift. If you look at the long-term trend, it doesn't go back to the long-term average.

- Difficulty predicting the future A deterministic trend is frequently mistaken for a chaotic system with a drift. While a random walk's value at time "t" (Yt-1) is regressed on the previous period's value (Yt-1), in the event of a constant term (t), it is regressed on the current period's trend (Yt-t) With nonstationary processes that have deterministic trends. The mean tends to rise and fall in lockstep with the trend.

- Roughly speaking, this is an example of the Randomized Stroll with Drift and Knowable Trend, which can be summarized as It's another nonstationary process that mixes random walk () and drift (t) with the deterministic trend (t). It includes a stochastic component, a drift, and the value from the previous period.

Stable trends and differences

Differentiating (deducting Yt-1 off Yt and calculating the difference between Yt and Yt-1) can change a stochastic process with or without a drift into a stationary process, which then becomes difference-stationary. The drawback is that one observation is lost each time a difference is taken.

Differencing

Detrending a nonstationary system with a time trend makes it stationary. As shown in the image below, a stationary process can be created by removing the trend from the equation: Yt - t = + t. A nonstationary process can be transformed into a stationary one by detrending.

Detrending

Even while detrending can eliminate both the drifting random walk and the determined trend, the random walk's variability will continue to grow indefinitely. As a result, stochastic trend removal requires the use of difference.

The Bottom Line

Unreliable and erroneous findings can be obtained using nonstationary time-series data in financial models. The problem can be solved easily when the data is transformed into stationary time series. Nonstationary processes can be turned stationary by differencing, even if they are random walks with or without drift. Detrending can be applied to time series data that demonstrates a deterministic trend to avoid erroneous results.

Detrending and differencing should be performed to nonstationary series to prevent generating misleading findings, as differencing will eliminate the stochastic trend in the volatility, and depleting will eliminate the deterministic one, respectively.